📊 No-code market making hits Polymarket

Plus: Arizona calls Kalshi a casino, and Congress moves to ban war bets

GM. You’re reading PredictionDesk, the daily newsletter that helps you become a prediction markets expert in under 5 minutes.

Here’s what we got for you today:

🚀 Facts.trade makes Polymarket market making point-and-click

🎰 Arizona alleges every Kalshi contract is an unlicensed bet, escalating state-level enforcement

💣 Murphy and Casar introduce bill criminalizing bets on military action and insider-controlled outcomes

📈 Market Moves

📊 Odds & Ends

MARKET MAKING ON POLYMARKET, NO CODE REQUIRED 🚀

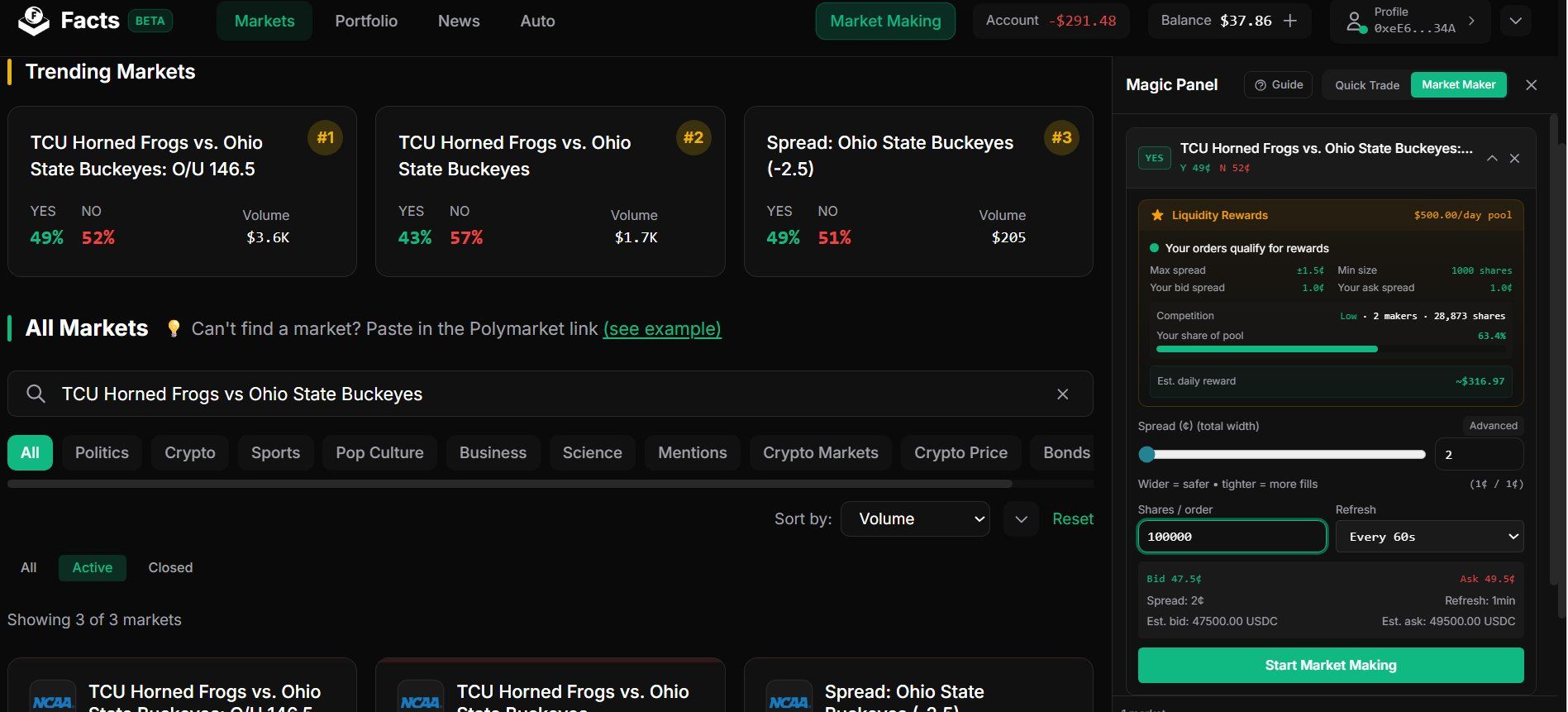

If you trade on Polymarket, you've probably noticed that some markets have tight spreads and deep liquidity while others feel like ghost towns. The difference is usually market makers, traders who place standing buy and sell orders and earn rewards from Polymarket for doing it. Until now, running a market making operation meant writing code and managing API connections. Facts.trade, a trading terminal built by the Polymarket-focused research group Polyfactual, just launched a feature called "Magic Panel" that lets you do it through a visual interface. You drag in up to five markets, set a spread with a slider, choose an order size and refresh interval, and the system automatically adjusts your orders to the latest mid-price every cycle, whether that's every 60 seconds or every 10 minutes.

The panel also shows you the economics before you commit any capital. You can see how many other makers are active on a given market, what share of the liquidity pool you'd capture, and what your projected daily earnings look like. On a market like "US strikes Iran by February 28, 2026?" with seven makers and roughly 115,000 shares, the panel was estimating around $413/day from a $1,000/day reward pool. That kind of visibility makes it much easier to figure out which markets are actually worth providing liquidity on versus which ones are already crowded.

Polymarket's liquidity reward program has historically been something only technically sophisticated traders could take advantage of. You needed custom scripts, API keys, and the time to monitor positions. Facts.trade's Magic Panel puts that same workflow into a GUI that anyone comfortable with a trading interface can use, which opens up reward income to a much wider group of participants.

Polyfactual's longer-term vision goes further than just making market making easier. They've been writing about graphical model market makers, a framework where related prediction markets (elections, Fed policy, inflation, recession odds) would be priced as a connected probabilistic network instead of independent contracts. If a trader moves the price on a rate hike market, inflation and recession markets would adjust automatically based on the encoded relationships between those variables. Right now, those inconsistencies between correlated Polymarket contracts only get corrected through manual arbitrage.

For Polymarket itself, tools like this address a real structural need. The platform's growth depends on consistent liquidity across hundreds of markets, and today that liquidity comes from a thin layer of power users running custom bots. If Facts.trade brings in enough new market makers by lowering the technical barrier, it strengthens Polymarket's core infrastructure without Polymarket having to build any of it. The prediction markets ecosystem is developing its own middleware layer, and Polyfactual is building a meaningful piece of it.

ARIZONA BETS KALSHI IS JUST GAMBLING 🎰

Arizona Attorney General Kris Mayes filed 20 misdemeanor criminal charges against KalshiEx LLC and Kalshi Trading LLC in Maricopa County Superior Court today, alleging the company ran an illegal gambling operation and accepted unlawful election bets from Arizona residents. No state has brought criminal charges against Kalshi before. Until now, the pushback has come through cease-and-desist letters, civil injunctions, and regulatory rulings.

Sixteen counts fall under Arizona's general gambling statute, which prohibits accepting bets on "any unknown or contingent future event." Four more target election wagering specifically, under a separate law that criminalizes accepting bets on election outcomes. The transactions prosecutors cited are small - a $30 bet on Commanders vs. Giants, $1 player props on Jaxon Smith-Njigba scoring the first Super Bowl touchdown, a $2 bet on J.D. Vance winning the 2028 presidential election, a $1 bet on whether the SAVE Act becomes law. Arizona isn't alleging fraud or massive losses. It's arguing that every event contract Kalshi offers is, under state law, simply a bet - and offering bets without a license is a crime.

Kalshi tried to get ahead of the filing by suing in federal court for a temporary restraining order. U.S. District Judge Michael Liburdi denied it, clearing the path for Mayes to act. That a federal judge wasn't persuaded - even at the preliminary stage - that CFTC jurisdiction blocks state criminal prosecution is a rough signal for Kalshi's preemption theory.

"Kalshi may brand itself as a 'prediction market,' but what it's actually doing is running an illegal gambling operation and taking bets on Arizona elections," Mayes said. Kalshi called the charges "paper-thin arguments" and maintained that its CFTC-regulated contracts fall under exclusive federal jurisdiction. But criminal exposure is a different animal than a regulatory letter, and the four election-wagering counts are the most dangerous part of the filing. They sit under a statute aimed at protecting election integrity, not regulating financial products - and preempting that with a derivatives license is a much harder argument to sell.

Massachusetts secured an injunction on sports contracts. Nevada applied state gaming rules. Now Arizona has filed criminal charges. Each state is building on the last, and the enforcement tools are escalating. If these election-wagering charges survive a motion to dismiss, AGs in other states with similar statutes will have a roadmap - and Kalshi will be fighting not just regulatory actions, but criminal cases, in courts where the CFTC's jurisdiction carries a lot less weight.

YOU CAN BET ON RATES BUT NOT ON RAIDS 💣

Senator Chris Murphy (D-CT) and Rep. Greg Casar (D-TX) introduced the BETS OFF Act today, a bill that would make it illegal for anyone to place, accept, or facilitate a wager on acts of terrorism, assassinations, wars, or non-financial government actions where insiders could have advance knowledge or control over the outcome. It's not a disclosure regime or an insider-trading rule. It's a categorical ban.

In the hours before the late-February U.S.-Israel strikes on Iran, 150 new accounts appeared on Polymarket, with 109 wagering more than $10,000 each. One trader, going by "Magamyman," reportedly made over $550,000 by betting on the exact date military action would begin. Murphy alleged the bets "must have come either from the White House or someone close." The White House denied it.

The drafting move that matters is the "specified event" definition. The bill bans wagers on any event whose "primary underlying characteristic is not financial, commercial, or economic" when the outcome involves government action, is under someone's control, or is known in advance. That carveout is carefully constructed: markets on interest rates, economic data, and commercial outcomes survive. Markets on whether the U.S. bombs Iran, who wins an Oscar, or what surprise halftime act the NFL books do not.

Beyond amending the Commodity Exchange Act to bar CFTC-registered exchanges from listing these contracts, the bill plugs its prohibitions into the Travel Act, the illegal gambling business statute, and UIGEA, classifying banned prediction market activity as gambling for federal criminal purposes. Enforcement runs through the Attorney General, and the whole thing would take effect 30 days after passage.

I think the drafting is smarter than it looks at first glance. By preserving markets with a financial or economic primary characteristic, Murphy and Casar are conceding ground the industry actually wants to hold: rate contracts, inflation markets, economic indicators. The real target is the category that generates the most public outrage and the weakest "price discovery" argument: betting on whether your government kills someone. Whether the BETS OFF Act passes is another question entirely. But the framework it proposes, banning the most indefensible contract categories while leaving the financial ones alone, is the kind of line that could attract bipartisan support if prior-knowledge allegations keep piling up.

MARKET MOVES 📈

📈 Biggest swing: "Will Indianapolis Colts win the 2027 NFL AFC Championship?" moved 1% -> 9% (Polymarket)

💰 Top earner: @reachingthesky -- $3,223,094 24H Profit (Polymarket)

🤔 Weirdest market: "Will MrBeast win the 2028 Democratic presidential nomination?" at 1% odds (Polymarket)

ODDS & ENDS 📊

Large banks including JPMorgan are beginning to extend insider-trading compliance frameworks to employee activity on Kalshi and Polymarket, a sign Wall Street is treating event contracts seriously enough to warrant the same guardrails as traditional securities.

MEXC is rolling out a zero-fee prediction-markets product on its centralized exchange, joining a growing wave of major crypto exchanges building event-contract features into their core trading platforms.

Bots are increasingly driving profits on Polymarket, exploiting latency and structural arbitrage rather than superior forecasting - raising questions about whether prediction markets are measuring crowd wisdom or execution speed.

RATE TODAY’S EDITION

Go from AI overwhelmed to AI savvy professional

AI will eliminate 300 million jobs in the next 5 years.

Yours doesn't have to be one of them.

Here's how to future-proof your career:

Join the Superhuman AI newsletter - read by 1M+ professionals

Learn AI skills in 3 mins a day

Become the AI expert on your team